The exit poll is pointing to a huge Labour majority and Sir Keir Starmer is readying himself to pick up the keys to Number 10.

Across Britain, panic will already be setting in for those who are concerned about the party’s future tax plans.

Rachel Reeves has previously tried to recast Labour as the party of growth, hinting at cuts for “working people”, including those paying the highest 45p rate.

It came after a multi-year campaign of Tory stealth taxes that will leave Britons buckling under the heaviest tax burden since the 1940s.

However, Labour’s manifesto – launched in mid-June and entitled simply “Change” – does not contain any tax cuts. It does commit the party to not raising National Insurance, income tax or VAT, but mentions nothing about other taxes that could be in the crosshairs if a new Labour government needs to raise revenue.

The months of uncertainty have left many middle-class Britons worried about what a Labour government would mean for their money, with some already rearranging their financial affairs.

Here, Telegraph Money details the taxes you could face under the new Labour government and what steps you can take now to protect your cash.

How much tax will I pay under Labour?

Labour has committed to not increasing income tax, National Insurance (NI) or VAT in its manifesto. Yet the Institute for Fiscal Studies (IFS) says that whichever party wins the general election, the new government will either need to raise taxes or cut spending in order to meet its own fiscal targets.

This raises questions about the cost of Labour’s spending plans and how it would bridge the gap – including whether it would raise other taxes to do so.

Labour says it will maintain the freeze on income tax thresholds, dragging millions more people into higher tax bands. It will mean all taxpayers pay more as their earnings increase, while the Office for Budget Responsibility estimates four million more will start paying by 2028-29.

The party has also refused to commit to ensuring tax does not become due on state pension income, which could lead to a three-figure yearly bill for those drawing the benefit.

There is also little comfort for second homeowners. After repeatedly declining to rule out increases to capital gains tax (CGT), there is no mention of it in Labour’s manifesto.

A future CGT rise could hit those with another property hard, with some experts believing a rise would be “tempting” for Labour – even though relief has already been cut significantly under the Conservatives.

There has also been speculation that a wealth tax could be introduced, levying a 2pc charge on the super-rich. However, such a move under Labour could completely backfire.

Finally, for those hoping to tax-efficiently leave their estates to their family and loved ones could come unstuck amid rumours of further IHT levies to come, as a leaked recording suggested Labour may seek to use the tax to “redistribute” wealth.

VAT on school fees confirmed

Sir Keir Starmer’s confirmed plans to scrap the VAT exemption for private schools, as well as applying business rates, is forcing taxpayers into life-changing financial decisions. The move could mean fees rising by 20pc as schools feel compelled to pass on the cost to parents.

The average day school fee in Britain is £18,063 per year, while the average boarding school fee is £42,459, according to the Independent Schools Council (ISC), a trade body.

Telegraph research has found that parents at almost a quarter of day schools would face fees of more than £30,000 if schools pass on their increased costs.

Sending three children to a private day school between the ages of five and 18 will cost £800,000 on average, according to digital wealth manager Moneyfarm. If VAT is added to these fees, it would mean parents having to find an extra £160,000 over the course of their children’s education.

This may prove too steep for some.

“Parents are very worried,” says Silas Edmonds, headmaster of Ewell Castle in Epsom, Surrey.

“It’s a very real attack. Many are already pulling their children out of private schools because they can’t afford fees.”

Mr Edmonds insists that the “stereotypical image” of private school children – boys from Eton in top hats and tails – is misleading.

“The reality is very different. Those schools that are the preserve of the super-rich charging fees of £40,000 a year won’t be affected at all [by the VAT hit].

“But the majority of independent schools are far more modest. Some are charitable trusts on very, very tight margins. Parents are making significant sacrifices to afford the school fees.”

Mr Edmonds’ school, where fees range from £3,695 to £6,731 per term, has around 680 pupils, but it would be “struggling”, he says, if numbers dropped by “even 30 or 40”.

The cost of energy bills, the five percentage point rise in teacher pension contributions due to come in from April, and the touted VAT charge are creating a “perfect storm”, threatening the viability of private schools.

“We’re being squeezed from every angle.”

An ISC survey found that 20pc of parents “would definitely” withdraw their children if VAT were added to school fees. This would put extra strain on the state sector which would be forced to absorb the pupils.

Whether parents follow through is another matter. Luke Sibieta, a senior research fellow at the Institute for Fiscal Studies (IFS), has said a mass exodus of private school pupils after the VAT fee hits is “incredibly unlikely”.

Even so, the ISC has warned that the greatest impact will be felt by “strivers and sacrificers” who work hardest to pay the fees. The move would also threaten “the survival of the smallest independent schools, which operate on tight margins and without large endowments”.

One option open to more fortunate parents would be to ask grandparents to transfer a chunk of their wealth to ease the burden.

The upside is that transfers made for the education of children are free from inheritance tax – but only if made by the parent.

So if a grandparent gifts a parent a lump sum, it will need to fall outside the “seven-year window” before a grandparent dies to be free of inheritance tax.

Otherwise, grandparents could make gifts out of their surplus income to benefit from the little-used “unlimited gifting” rule that means the seven-year period will not apply.

Mr Cook is advising one of his clients to consider drawing down a chunk of money in his pension to pay for the expected hike in his grandchildren’s school fees.

“It’s not a way of mitigating the tax,” he says. “But it’s a way of dealing with the problem.”

Taking these sorts of decisions is having a “huge” impact on people in similar positions.

“It may be that later in life [the client] has to forego his own standard of living. The money he’s using to keep his children in private education might well mean there’s less available if he goes into long-term care later in life.”

Parents had hoped that paying fees in advance would allow them to dodge the VAT hit. But Bridget Phillipson, the shadow education secretary, has said Labour’s legislation would be “drawn in such a way to ensure that avoidance can’t take place”.

She suggested that VAT would still apply to payments made before Labour abolished the tax exemption if the payments were made for schooling that takes place after the policy has been introduced.

Closing the early-pay loophole leaves parents with very few options, and the onus will fall on schools to find ways to avoid passing on the full cost.

Private schools may have to resort to trimming the number of bursaries they offer, Mr Edmonds says.

“The irony of Labour’s policy is that they think by spanking the independent schools they’re going to help social mobility.

“In actual fact, for the children at our school, some of whom are on full bursaries if they’re from particularly challenging backgrounds, suddenly social mobility is off the table.”

‘Non-dom’ rules scrapped

The potential for Labour’s tax policies to backfire extends to so-called “non-doms”.

The “non-domiciled” tax regime, which lets wealthy individuals earn foreign income tax-free for up to 15 years, will be scrapped “once and for all” according to its manifesto.

Labour claims that forcing non-doms to pay tax on their foreign income could net the Treasury £3.5bn a year.

Yet if non-doms decide to up sticks and leave Britain, they will take their large tax bills with them. Many have already done so, attracted to sunnier, lower tax regimes in the United Arab Emirates and United States.

Some 37,000 non-doms paid £6.2bn in tax in 2020-21, according to HM Revenue & Customs, meaning they paid around £167,000 each on average in income tax, capital gains tax and National Insurance contributions combined.

By comparison, the average tax liability per UK worker last year was just over £7,000, excluding capital gains tax.

David Lesperance, a tax expert who advises wealthy expats, says his high net-worth non-dom clients are “fine-tuning their escape plans” in anticipation of a Labour government.

But for non-doms wanting to swerve UK tax, moving abroad isn’t the only option.

Sheltering investment portfolios in an offshore insurance bond could be a good idea for those who are confident they will become a basic-rate taxpayer or move to a low-tax jurisdiction later in life.

The income and gains of the bond are not taxed as they arise. However, an exit strategy should be carefully planned to avoid paying income tax on the bond at the higher rate.

An alternative would be to invest for capital growth, rather than income, which could bring assets out of the income tax regime and into capital gains tax.

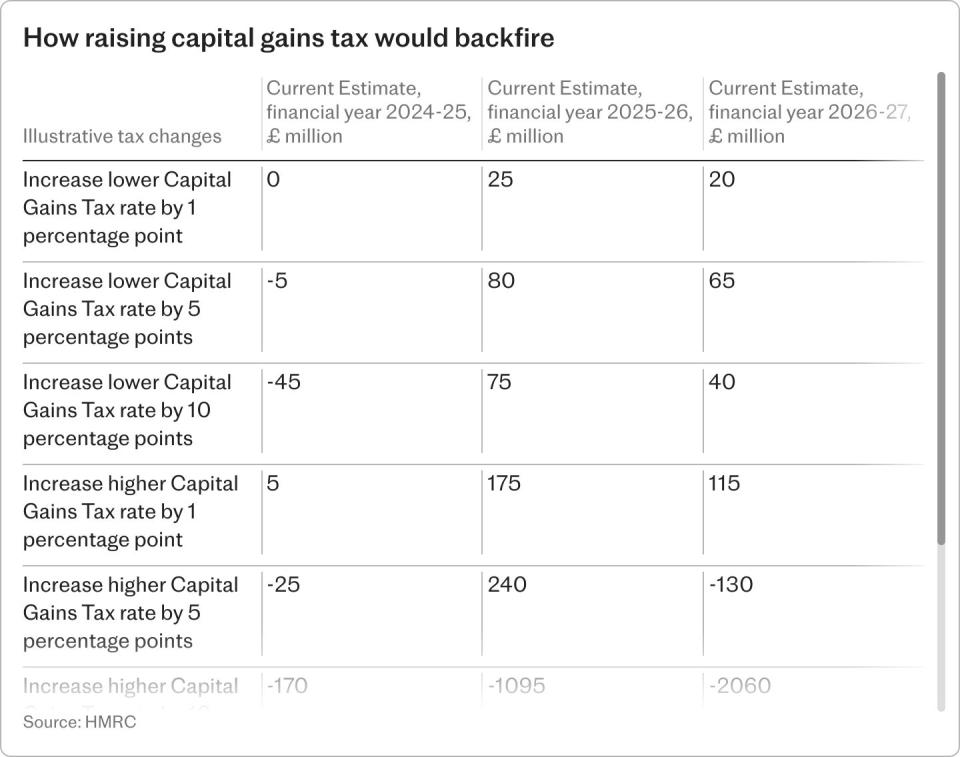

Doing so would make sense, unless Labour decides to raise capital gains tax – a move Ms Reeves has refused to deny.

“I think a capital gains tax rise would be very tempting for Labour,” says Chris Etherington, of accounting firm RSM.

“As it stands, it doesn’t look like many of Labour’s plans – like VAT on private school fees or changes to non-doms – are going to generate a lot of headroom for spending. So they’re going to look elsewhere.”

Basic-rate taxpayers currently pay 18pc on their profits from the sale of a second home and 10pc for shares, while higher-rate taxpayers pay 24pc and 20pc.

The Conservatives have already dramatically scaled back relief given to sales and payouts that incur capital gains and dividend taxes.

But a hike in the headline rate would “really distort” taxpayer behaviour, Mr Etherington warns.

“If Labour were to put it up, people would take action.”

While business owners are usually hit hardest by a capital gains tax hike, landlords would be an “easy target”, he says, if Labour were to “experiment with who should suffer first”.

“You’d probably see more landlords selling up. They’ve seen a lot of tax changes over the last few years. It could be the final nail in the coffin.”

The capital gains tax allowance halved from £6,000 to £3,000 in April.

Giving assets to family members who are basic-rate taxpayers is another way to avoid paying capital gains tax at the higher rates of 20pc and 24pc.

If you own shares and see a capital gains tax rise coming down the track, it’s worth considering a so-called “bed and breakfast” deal, according to Mr Etherington.

This involves selling the shares, triggering capital gains tax at the current (lower) rate, before re-buying the shares 30 days later, and avoiding a higher liability further down the line.

Inheritance tax could be on the table

There were also concerns that inheritance tax rules could also be tightened, making it harder for the elderly to leave money to their families after they die without incurring a levy.

However, the manifesto only included a commitment to end the use of offshore trusts to avoid the charge.

A leaked recording of a shadow frontbencher has raised fears that the party could be planning a raid on family wealth after death. Darren Jones, the shadow chief secretary to the Treasury, told a public meeting in March that inheritance tax could be used to “redistribute wealth” and address “intergenerational inequality”.

This has raised fears that Labour could attack various reliefs that allow families to pay less inheritance tax.

Britain has one of the highest inheritance tax rates in the OECD at 40pc.

If your estate is worth more £325,000 when you die, then your beneficiaries will pay this charge on everything above the threshold, called the nil-rate band.

The tax-free exemption has been frozen at £325,000 since 2009, dragging thousands into the net as house prices have soared.

According to official forecasts, the number of families paying the charge will hit nearly 44,000 a year by 2028-29, up from 33,000 this year. In total, almost 200,000 will pay the tax over the next five years.

But the number could be even higher if Labour chooses to increase the tax burden.

Currently, homeowners can pass on £500,000 – or £1m if they are a couple – as long as they leave their house to their children. Labour could choose to cut or lower this exemption, widening the scope of inheritance tax.

In this case, it’s a good idea to make sure you’re clear on all the ways you can (legally) avoid inheritance tax – including making gifts and transferring wealth to your spouse.

Alternatively, Labour could attack various reliefs that allow people to give away their wealth earlier, without paying death duties.

No room for manoeuvre

Given the state of the public finances Labour is inheriting, the chances of the party introducing net tax cuts are vanishingly small.

But what if Ms Reeves’ tax-cutting hints are taken at face value?

She was thought to be weighing up plans to offer income tax or NI cuts in Labour’s manifesto, but it only includes a pledge not to raise either. It also commits to not raising VAT.

In terms of the taxes Labour could increase, Paul Johnson, director of the IFS, says the options are “as long as a piece of string”.

Owners of more expensive homes could face higher council tax bills, Mr Johnson says, a policy that would hit many current pensioners who tend to live in larger, more valuable homes.

An overhaul of the property tax could add hundreds to annual bills – with some facing rises of as much as £4,609, according to an Institute for Fiscal Studies (IFS) analysis of house prices.

Fears of a council tax raid are growing after a frontbencher implied the system “needs to be changed”.

In a leaked recording, Darren Jones, shadow chief secretary to the Treasury, told a constituency meeting that any party who suggested revaluing council tax bands “had never been elected”.

There were fears that Labour would cut tax relief on pension contributions for high earners, particularly after it was revealed Ms Reeves argued for a flat rate of 33pc for everyone back in 2016. However, a Labour Party spokesman said recently that there were “no plans” to change tax relief and there is no mention of it in the manifesto.

Income tax thresholds are frozen until 2027-28, and inflation is set to drag more than seven million people into higher income tax bands by the end of the decade as allowances fail to keep pace with price rises. Sir Keir has so far refused to commit to unfreezing these thresholds.

Background spending pressures on the NHS, welfare and pensions will mean the tax burden will continue to climb whoever wins the election, says John O’Connell, head of the Taxpayers’ Alliance. It will also make it difficult for Labour to stick to its pledges on wealth and income tax.

He adds: “Unless there’s significant reform on one or all of these ‘big three’, any government is going to struggle to get spending under control, so that they can deliver meaningful tax cuts.

“Labour saying they won’t put up headline rates on income tax is all well and good, but as we’ve seen with the current government, there are ways they can get around that to squeeze taxpayers more.”

Pension U-turn

Labour has previously been vague about its tax-and-spend plans, perhaps deliberately, even on the few proposals it had announced before the manifesto was released.

The lack of clarity made political sense, says Steve Webb, a former pensions minister, now of consultants Lane Clark and Peacock (LCP).

“The more specific you are, the easier it is to attack you. And good ideas can be nicked. All parties do it.”

But for those trying to plan their next financial move, the absence of detail has been “really unhelpful”, said Ian Cook, of wealth manager Quilter, especially for those 50-somethings with large pension pots.

At the Budget in March, Ms Reeves pounced on Jeremy Hunt’s announcement that he was abolishing the lifetime allowance (LTA). The change to pension rules was a “tax cut for the rich”, she said, and a Labour government would reverse it.

Since getting rid of the lifetime allowance, workers can now accumulate unlimited pension savings without having to pay additional tax, while those looking to retire can cash out up to £268,275, or 25pc of the old lifetime allowance, tax free.

Previously, accessed pension savings over the lifetime limit were subject to a tax charge of up to 55pc.

Labour’s initial pledge to reinstate the cap sparked a rush among those approaching pension age to cash in on any savings over the limit, before the old tax regime – or a new version – could be imposed. Experts also warned that pension savers were making decisions based on speculation.

However, the party has since reportedly U-turned on its plan and says it will now not reintroduce it.

If Labour were to U-turn again, a reintroduction of the LTA could affect up to 6pc of savers with pension funds approaching retirement, or around 250,000 people, LCP analysis shows. This number could snowball as wage inflation and investment growth carry thousands more over the threshold.

One saving grace is that any Labour reform to the pension system won’t kick in straight away.

“Any change wouldn’t happen quickly. The Government would have to announce any changes in their first budget, and then consult on them.

“It would be the following tax year at the very earliest before it comes in, so there will probably be one to two years to adjust. At the very longest, this might be at the end of a new Parliament.”

Broaden your horizons with award-winning British journalism. Try The Telegraph free for 3 months with unlimited access to our award-winning website, exclusive app, money-saving offers and more.